Spring Forecast summary 2026

By Amal Shah

04 Mar 2026

We are delighted to release our summary of the key announcements in the Spring Forecast 2026.

Contents

- Spring Forecast highlights.

- Spring 2026 – a challenging context.

- Economic background.

- Spring Forecast 2026.

Spring Forecast highlights

- The Office for Budget Responsibility (OBR) revised the UK’s GDP growth forecast down to about 1.1 % in 2026, with expectations that growth will pick up to around 1.6 % in 2027/2028.

- Income tax, National Insurance and VAT rates will stay in place, leaving major tax decisions to the upcoming Autumn Budget.

- Public sector borrowing is expected to be lower than earlier forecasts by about £18 billion, and fiscal headroom has increased, reducing immediate pressure for additional tax measures in the short term.

- Unemployment is projected to peak in 2026 before falling over the rest of the forecast period, indicating continuing labour market pressures this year.

Spring 2026 – a challenging context

It has been an eventful few months, with U-turns on both the 2024 Budget measures relating to Inheritance Tax (IHT) agricultural and business reliefs and the 2025 Budget proposals for business rates. And that is before the political storms of the winter are considered, which have had their own economic impact via the uncertainty created.

The current flare up of hostilities in the Middle East may, as the Office for Budget Responsibility notes, have “very significant impacts on the global and UK economies”. In turn that could call into question the Forecast numbers. With oil prices already affected and the stock and bond markets reacting negatively to the uncertainty created, the Chancellor will be hoping the repercussions do not prove too serious for UK plc by the time of her next Budget this autumn.

Economic background

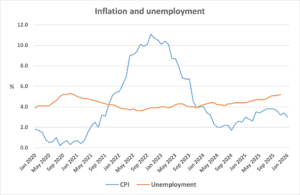

The Autumn 2025 Budget took place against a backdrop of UK GDP growth having slowed to just 0.1% in the third quarter, after starting the year with a first quarter reading of 0.7%. Preliminary figures from the Office for National Statistics (ONS) released in mid-February 2026, suggested GDP growth remained at 0.1% in the final quarter and that 2025 GDP growth was 1.3%. In the same month, the ONS also published its usual monthly data on the labour market, inflation and retail sales:

- Unemployment for October to December 2025 was 5.2%, up from 4.4% for the corresponding period a year ago and above pre-coronavirus pandemic rates. The hardest hit were those aged 16 to 24, where the unemployment rate was 16.1%, the highest for over a decade.

- Average weekly earnings annual growth (with and without bonuses) was 4.2%, down from 5.9% for October to December 2024. However, the latest figure is distorted by the bunching of public sector pay settlements – the private sector earnings growth (with and without bonuses) was 3.5%.

- Annual CPI inflation was 3.0% in January 2026, unchanged from a year ago. The Bank of England, along with many independent forecasters, anticipate that inflation will be close to the Bank’s 2.0% by April.

- The volume of retail sales rose by 0.1% in the three months to January 2026, compared with the previous three months. However, January alone saw a 1.8% rise with the ONS noting there was ‘a good start to the year for non-food stores’. This came on top of a 0.4% rise in December and a 0.4% November drop – probably attributable to that late Budget.

Mixed economic data is less of a problem for the government’s finances than it would have been a year ago, thanks to the Chancellor’s decision in November 2025 to build an extra £11.8 billion into her fiscal headroom – the amount by which the government’s revenues are projected to exceed its day-to-day spending in 2029/30.

Source: Office for National Statistics

Spring Forecast 2026

OBR projections Autumn Budget 2025 vs Spring Forecast 2026

| OBR Projection | November 2025 | March 2026 |

| GDP Growth 2026 | 1.4% | 1.1% |

| GDP Growth 2027 | 1.5% | 1.6% |

| CPI Inflation 2026 | 2.5% | 2.3% |

| LFS* Unemployment 2026 | 4.9% | 5.3% |

| LFS* Unemployment 2027 | 4.6% | 4.9% |

| Average oil price per barrel 2026 | $64.38 | $63.09 |

| Bank Rate 2026/27 | 3.6% | 3.4% |

| Bank Rate 2027/28 | 3.7% | 3.6% |

| Weighted average gilt yield 2026/27 | 4.7% | 4.5% |

| Weighted average gilt yield 2027/28 | 4.9% | 4.8% |

| Fiscal headroom 2029/30 | £21.7 billion | £23.6 billion |

| Public sector net financial liabilities 2029/30 | 83.0% GDP | 82.2% GDP |

| Public sector net borrowing 2026/27 | £112.1 billion | £115.5 billion |

*Labour Force Survey, Source: Office for Budget Responsibility

With little more than three months since the OBR published (slightly prematurely…) its last Economic and Fiscal Outlook (EFO), it was likely there would be few significant changes in the numbers.

Growth

As the table above shows, the OBR’S projection for economic growth in the current year has been cut to 1.1%, bringing it into line with the February market consensus, but still above last month’s Bank of England’s forecast of 0.9%. The OBR increased its projections for growth in both 2027 and 2028 to 1.6% (from 1.5%), largely countering the impact of its 2026 reduction over its five-year forecast period.

Inflation

The OBR’s inflation projection for this year was cut by 0.2% to 2.3%, which closely matches the Bank of England’s own estimate for inflation. To a degree this fall of inflation has been engineered by the government with the actions it has taken on administered prices, such as the energy price cap and rail fares.

Unemployment

The better outlook for inflation may also be due in part to a gloomier projection for unemployment, which the OBR now sees as averaging 5.3% in 2026, against the 4.9% which it projected back in November 2025. Unemployment stays above those previous EFO levels until 2029, by which time it is projected to have fallen back down to 4.2%, marginally below where it was in 2024.

Fiscal headroom

Fiscal headroom, which caused so much angst for the Chancellor a year ago, barely received a mention in her speech. The ‘stability rule’ headroom – the extent to which the current budget is projected to be in surplus by 2029/30 – rose from £21.7 billion to £23.6 billion. The increase was the result of a mix of factors, including:

- Revisions to the OBR’s assumptions, such as on interest rates.

- Buoyant tax receipts, visible in the record £30.4 billion January surplus recently reported by the Treasury.

- Increased spending on special educational needs and disabilities (SEND), averaging £4.2 billion a year between 2028/29 and 2030/31.

- Other increased spending, such as the cost of rejoining the Erasmus programme.

- The costs of U-turns on IHT reliefs and business rates for pubs and live music venues. For all the attention these received, the loss of revenue is estimated to be an average £0.1 billion a year for each.

Borrowing

Government borrowing for the current year is now projected to be £132.7 billion, down £5.5 billion from the OBR’s November 2025 number, but £15 billion more than it projected a year ago. 2026/27’s borrowing is projected to be £115.5 billion, 3.1% higher than projected in November. Thereafter borrowing is below November’s projections.

Gilts

The uptick in borrowing contrasts with a £51.6 billion drop in projected gilt sales to £252.1 billion in 2026/27. Over half that decline stems from £27.5 billion less in gilt redemptions requiring refinancing in the next financial year. Net debt interest in 2026/27 is projected to be £109.4 billion, £3.9 billion below the November forecast, thanks to lower inflation and interest rates.

Middle East conflict

All these projections come with an obvious, elephant-sized caveat. To quote the OBR from the EFO’s executive summary, “Conflict in the Middle East, which escalated as we were finalising this document, could have very significant impacts on the global and UK economies”. On Tuesday Brent crude was trading at close to $84 a barrel, over $20 above the OBR’s forecast for the 2026 average price.

The gilts market also underlined that OBR caution on Tuesday 3 March, with the yield on the ten-year gilt rising to 4.57% from 4.39% at close on Monday. At the same time money markets movements suggested hopes that the Bank of England would cut bank rate later this month have largely faded.

There are now about eight months until the Budget, by which time the next round of OBR figures could be more challenging than the spring’s set.

We’re here to help

If you have any questions relating to the announcements made in the Spring Forecast Statement, please get in touch with one of our expert Tax Advisers.

Let’s get started

Contact page

Contact Us